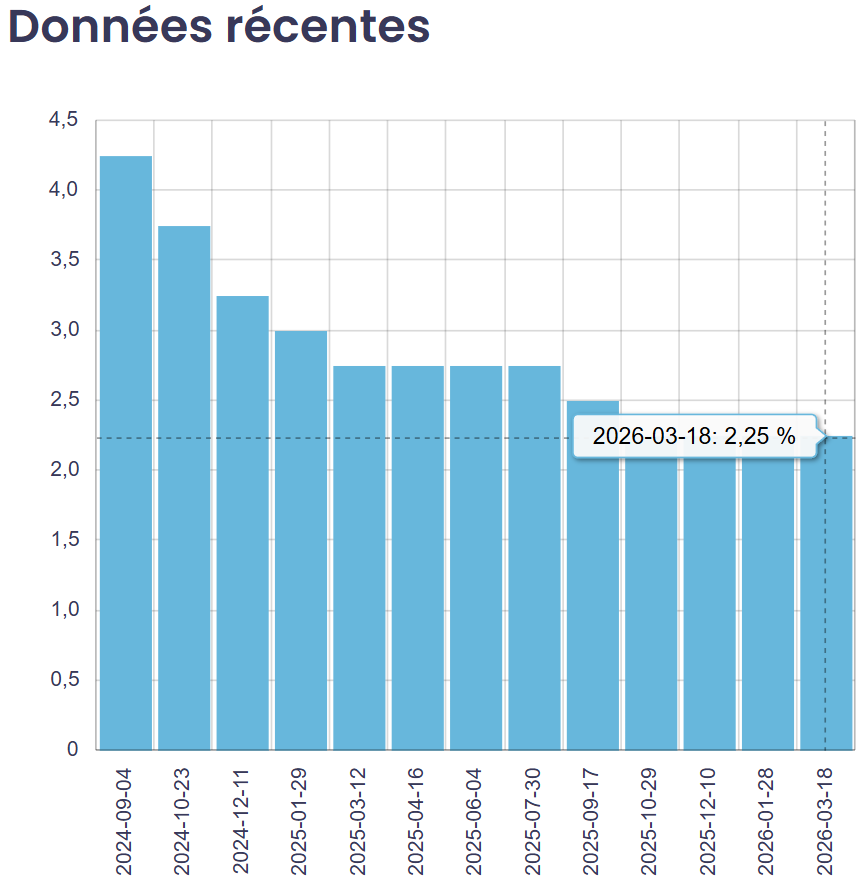

This morning, March 18, 2026, the Bank of Canada announced that it is maintaining its key policy rate at 2.25%.

This decision comes amid a context of heightened economic uncertainty. The war in the Middle East has increased volatility in energy prices and financial markets, while the Canadian economy contracted by 0.6% in the fourth quarter of 2025, following growth of 2.4% in the previous quarter. Domestic demand remains solid, supported by consumer spending and government expenditures, while the housing market continues to be weak.

Headline inflation slowed to 1.8% in February, and core inflation remains close to the 2% target. The Bank of Canada noted that risks to growth are tilted to the downside, while risks to inflation have increased due to higher energy prices.

The Bank remains prepared to adjust its monetary policy in response to evolving economic and global conditions. The next policy rate announcement is scheduled for April 29, 2026, along with the Monetary Policy Report. We will continue to closely monitor economic developments and their impact on the mortgage market.

Implications

The Bank of Canada’s target for the overnight rate determines the prime rate set by major financial institutions, which is the benchmark used to price variable-rate mortgages. Therefore, today’s announcement is not expected to change the rates currently offered on variable-rate mortgage loans.

However, the Bank of Canada’s policy rate does not directly determine fixed mortgage rates.

Why use a mortgage broker?

In a context where decisions by the Bank of Canada are becoming increasingly difficult to anticipate, it is more important than ever to rely on an expert. A mortgage broker can help you understand the impact of changes in the policy rate on your financing strategy and guide you toward an option that suits your situation—whether you are purchasing a home, renewing your mortgage, or refinancing.