A look back at the Radio-Canada News article titled “The Bank of Canada believes it may be able to lower interest rates ‘sometime during the year’.”

LOn March 6, the Bank of Canada decided to keep its key interest rate at 5% and is considering lowering it later in the year. Governor Tiff Macklem explained that the central bank wants to avoid acting too quickly, in order not to have to reverse course afterward. However, members of the governing council have openly expressed the possibility of an imminent rate cut if the economy and inflation evolve in line with the Bank of Canada’s projections.

This Wednesday, the U.S. Federal Reserve also announced that it was keeping its benchmark interest rate unchanged for the fifth consecutive meeting.

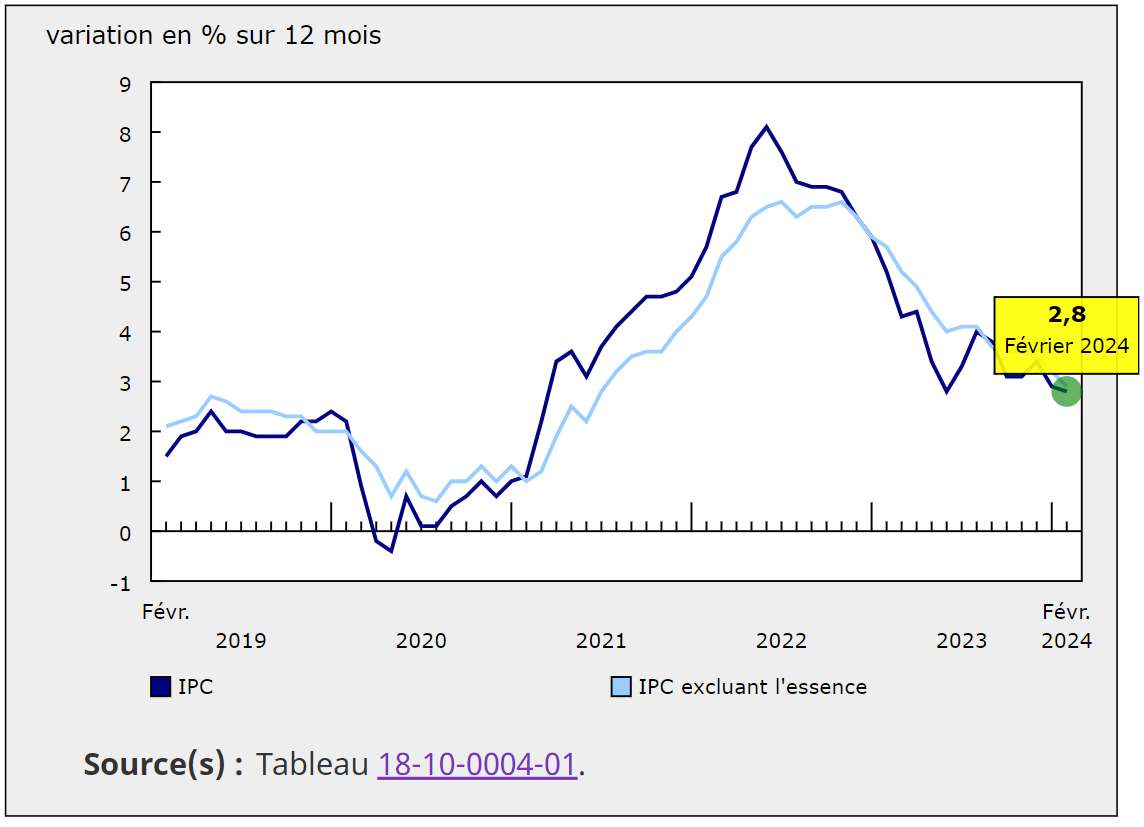

In Canada, inflation came in lower for the second month in a row, recording a rate of 2.8% in February. These recent figures have strengthened economists’ belief that the Bank of Canada will begin cutting its key interest rate around mid-year. However, the published deliberations on Wednesday suggest that the central bank remains highly concerned about the risk of higher-than-expected inflation, mainly driven by persistently rising housing costs.

This announcement echoes a La Presse article, which highlights that one of the central bank’s main concerns is housing costs—including mortgage interest and rent—which continue to contribute to inflation. They also note that while mortgage interest can influence inflation, its impact is not permanent, as interest rates are expected to eventually decline. As a result, policymakers believe they may be able to overlook this effect to avoid slowing the economy if mortgage interest were the sole driver of lower inflation, though they do not believe this is currently the case.

The Bank of Canada was also anticipating a rebound in the housing market in the spring, a trend that appears to be confirmed by recent home resale statistics. The governing council is concerned that if the housing sector rebounds in the spring, it could further drive up housing costs, delaying the return of inflation as measured by the CPI to the 2% target.

The next Bank of Canada interest rate announcement is scheduled for April 10. At that time, we will see whether the central bank’s concerns about housing have eased enough for it to officially consider the long-awaited interest rate cuts.

The key interest rate acts as a benchmark that guides financial institutions in setting their prime lending rates. As such, contact a mortgage broker to help you better understand the advantages of variable versus fixed rates, as well as the different products available to provide you with maximum flexibility in an ever-changing market.

To learn more, see the following article: Everything you need to know about fixed-payment variable rates.