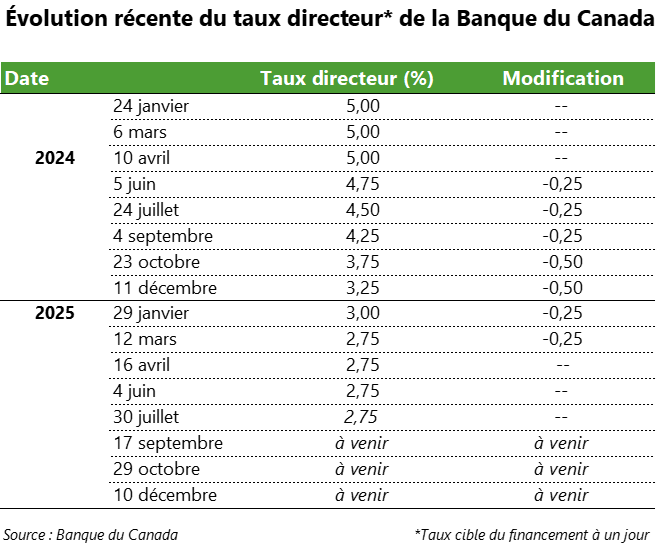

For a third consecutive meeting, the Bank of Canada has decided this morning to keep its target for the overnight rate at 2.75%. It is worth recalling that the last rate cut (-0.25 percentage points) dates back to March 12.

The Governing Council justifies its decision to hold the rate steady in a context where, despite high uncertainty, the Canadian economy shows some resilience, while inflationary pressures persist. However, the Bank is leaving the door open to possible further rate cuts: “If weaker economic conditions put additional downward pressure on inflation and trade-related price disruptions remain contained, a reduction in the policy rate may become necessary.”

In its statement, the Bank highlights the following conditions in Canada’s economic environment: 1) U.S. tariffs are disrupting trade, but overall the economy remains relatively resilient so far; 2) growth in business and household spending is being restrained by uncertainty; 3) labour market conditions are weakening in trade-exposed sectors, while employment remains stable in the rest of the economy.

The Bank also notes that inflation, as measured by the Consumer Price Index (CPI), stood at 1.9% in June, a slight increase from the previous month. However, excluding taxes, inflation rose to 2.5% in June, compared to about 2% in the second half of 2024. The sharp increase in housing costs remains the main driver of overall inflation, although it continues to slow.

Implications

The Bank of Canada’s target for the overnight rate determines the prime rate set by major financial institutions, which is the benchmark used to price variable-rate mortgage loans. Therefore, today’s announcement is not expected to change the rates currently offered on variable-rate mortgages.

However, the Bank of Canada’s policy rate does not directly determine fixed mortgage rates.

Why use a mortgage broker?

In a context where Bank of Canada decisions are increasingly difficult to anticipate, it is all the more important to rely on an expert. A mortgage broker can help you understand the impact of changes in the policy rate on your financing strategy and guide you toward an option that suits your situation, whether you are purchasing a home, renewing your mortgage, or refinancing.