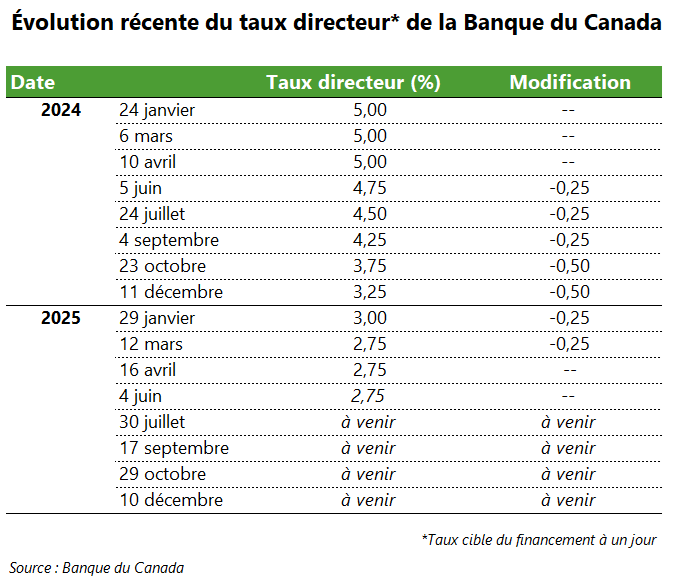

This morning, the Bank of Canada announced that it is maintaining its target overnight rate at 2.75%. Recall that on April 16, the Bank also held its policy rate steady, ending a series of seven consecutive cuts totaling 2.25 percentage points since June 5, 2024.

The Governing Council explained its decision by pointing to stronger-than-expected inflation. Although the Consumer Price Index inflation rate fell to 1.7% in April, this decline was mainly due to the removal of the federal carbon tax. Excluding taxes, inflation rose by 2.3% in April, and the Bank’s preferred core inflation measures also increased. In addition, tariffs are expected to eventually push prices higher.

The Bank also noted that Canada’s GDP growth in the first quarter (2.2%) was slightly stronger than anticipated. Front-loading of exports to the United States boosted activity, and business investment growth was higher than expected. However, the labour market weakened, particularly in export-oriented sectors, and the unemployment rate rose to 6.9% in April.

Finally, the Bank expects the economy to be significantly weaker in the second quarter.

Implications

The Bank of Canada’s target overnight rate guides the prime rate of major financial institutions, which in turn is linked to the interest rate they offer on variable-rate mortgage loans. Today’s announcement should therefore not change the rates offered on variable-rate mortgages.

However, the Bank of Canada’s policy rate does not directly determine fixed mortgage rates.

Why work with a mortgage broker?

In a context where Bank of Canada decisions are increasingly difficult to anticipate, it is all the more important to be able to rely on an expert. A mortgage broker can help you understand the impact of changes in the policy rate on your financing strategy and choose an option tailored to your situation, whether you are buying, renewing, or refinancing.