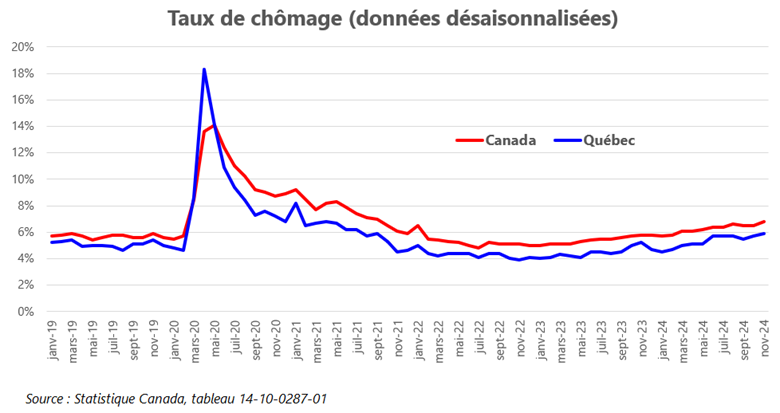

In November, Canada recorded an increase in its unemployment rate, reaching 6.8%, the highest since January 2017, excluding the pandemic period. Although 51,000 jobs were created, this increase is mainly due to a rise in the number of people looking for work. Quebec followed a similar trend with 22,000 new jobs, but an unemployment rate that rose to 5.9%, highlighting persistent imbalances between labour supply and demand.

This situation has significant implications for the Bank of Canada’s imminent decision regarding its policy interest rate. While the unemployment rate is an important factor, other economic indicators suggest that a cut in the policy rate is likely in order to stimulate economic growth. The key factors to consider are:

- Inflation under control: Inflation returned to the Bank of Canada’s 2% target range in October.

- Weak economic growth: GDP growth was weak in the third quarter, and GDP per capita has declined (-0.4%) for a sixth consecutive quarter.

- Main concern: economic growth and the labour market: The Bank of Canada is now focusing less on inflation control and more on sluggish economic growth and a cooling labour market.

- Slowing population growth: The federal plan to reduce the number of temporary immigrants could slow population growth, thereby weighing on overall economic growth.

Heading toward a cut in the policy interest rate?

All indicators appear to point toward another cut in the Bank of Canada’s policy interest rate this Wednesday, a move anticipated by several major financial institutions. The expected reduction could be as much as 0.5 percentage points, reflecting a desire to support economic growth and stimulate an already fragile labour market.

Impacts on mortgage rates

Such a decision will directly affect variable mortgage rates, which are expected to decline further. However, fixed rates—driven by other factors such as government bond yields—will not necessarily fall. Interest rates on fixed-rate mortgages can change by a very different magnitude and may sometimes even move in the opposite direction.

Outlook for 2025

The combination of falling interest rates and new mortgage rules allowing first-time homebuyers to extend their loan amortization period to 30 years is expected to revive the resale housing market. A strong return of first-time buyers is anticipated, with pent-up demand ready to be unlocked in a more favourable environment. However, the persistent imbalance between supply and demand will likely continue to put upward pressure on prices.