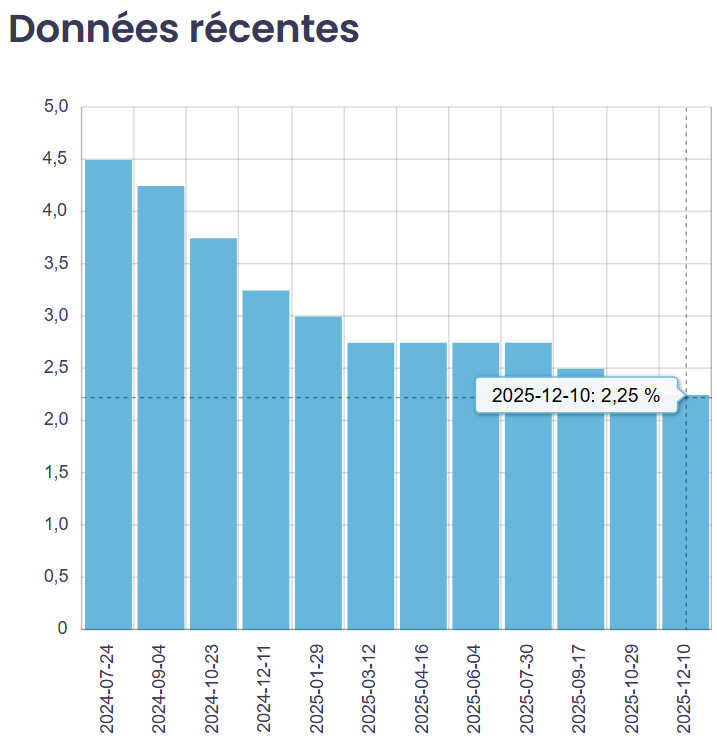

This morning, December 10, 2025, the Bank of Canada announced that it is maintaining its key policy rate at 2.25%.

The Governing Council believes that the current level of the rate remains appropriate to keep inflation close to the 2% target, while supporting a Canadian economy that is evolving in a context of elevated uncertainty and uneven growth across sectors.

On the global stage, major economies are showing resilience despite a more complex trade environment, particularly due to U.S. protectionist policies. In Canada, growth surprised to the upside in the third quarter, but the Bank expects a temporary slowdown in the short term before a gradual recovery in 2026.

The labour market is showing some signs of improvement, although hiring intentions remain moderate, while overall inflation continues to hover near the target, with short-term fluctuations expected.

The next policy rate announcement is scheduled for January 28, 2026. We will continue to closely monitor economic developments and their impact on the mortgage market.

Implications

The Bank of Canada’s target for the overnight rate determines the prime rate set by major financial institutions, which is the benchmark used to price variable-rate mortgages. Therefore, today’s announcement is not expected to change the rates currently offered on variable-rate mortgage loans.

However, the Bank of Canada’s policy rate does not directly determine fixed mortgage rates.

Why use a mortgage broker?

In a context where Bank of Canada decisions are increasingly difficult to anticipate, it is all the more important to rely on an expert. A mortgage broker can help you understand the impact of changes in the policy rate on your financing strategy and guide you toward an option that suits your situation, whether you are purchasing a home, renewing your mortgage, or refinancing.