Although mortgage rates have begun to decline in recent months, many borrowers are currently renewing their mortgages at higher interest rates. For example, a borrower who renewed their mortgage last October faced an increase of დაახლოებით 1.35 percentage points (based on the average posted rates of major financial institutions) if they had previously chosen a five-year fixed-rate loan.

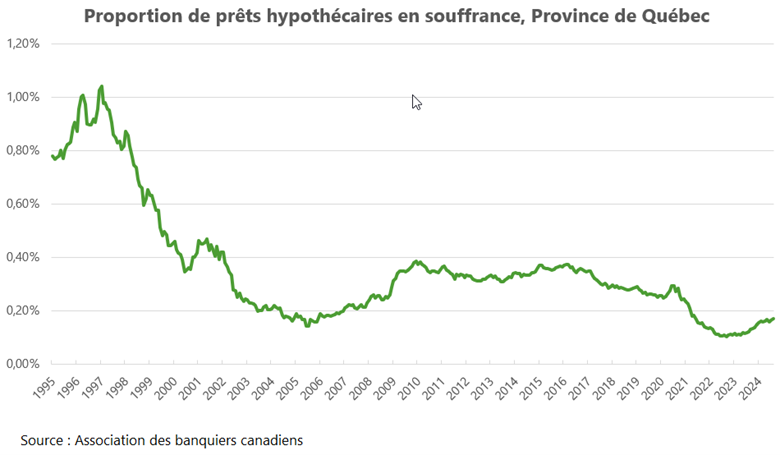

The number of mortgages in arrears—meaning payments are three months or more overdue—is currently rising across the country, and Quebec is no exception. According to the Canadian Bankers Association, over the course of a year, the proportion of residential mortgages in arrears in Quebec increased from 0.12% in August 2023 to 0.17% in August 2024 (roughly 1 in 600 mortgages).

From a historical perspective (see chart below), this level remains relatively low and is still well below pre-pandemic levels.nt faible et aussi nettement en deçà du niveau pré-pandémique.

However, there is still a significant wave of homeowners who will need to renew their mortgages at higher rates in 2025 and 2026. Many of them had benefited from exceptionally low mortgage rates five years earlier, when the pandemic pushed interest rates to historic lows. If you find yourself in this situation and anticipate difficulty meeting your payments, it’s best to act early.

As a first step, contact one of our mortgage brokers several months before your renewal date. They can advise you on various options (variable vs. fixed rates, term length, amortization period, etc.) and present different future payment scenarios. They can also shop around on your behalf to secure the best possible terms from different lenders for your renewal. In some cases, refinancing may also be an option, which is made easier by the fact that property values in Quebec have increased by an average of 40% since 2019. This means you have likely built up significant equity (the difference between your property’s value and your remaining mortgage balance).

Additionally, before you fall into mortgage default (and damage your credit record), it is often possible to obtain payment relief from your lender.

In particular, if you have an insured mortgage (i.e., you made a down payment of less than 20% when purchasing your property), mortgage insurers (CMHC, Sagen, and Canada Guaranty) all offer assistance programs for owner-occupiers experiencing temporary financial difficulties.

For example, arrangements may include payment deferrals, adding arrears to your remaining loan balance, or extending the amortization period. Under the new Canadian Mortgage Charter, lenders are also expected, in cases of severe financial hardship, to allow the sale of your primary residence without prepayment penalties.

Finally, in all cases, make sure to prioritize your mortgage payments over other forms of credit such as credit cards, auto loans, or lines of credit.

These tips may help you avoid reaching a last-resort situation—having to hand over the keys of your property to the lender.

[1] However, these statistics do not include credit unions such as Desjardins.

[2] Limited to a maximum of 80% of your property’s market value.