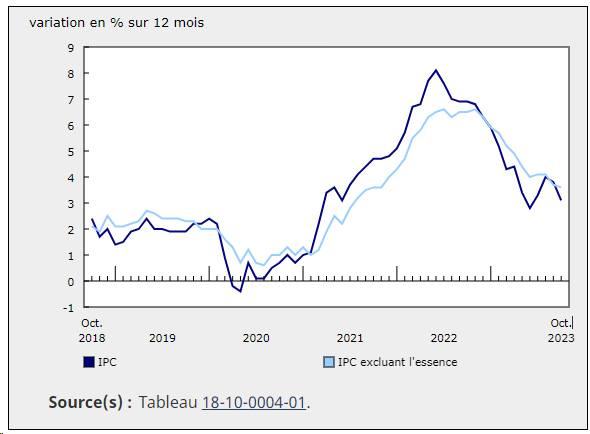

Recently, Statistics Canada released inflation data (The Daily — Consumer Price Index, October 2023 (statcan.gc.ca)). The key inflation indicator dropped from 3.8% to 3.1% in one month, suggesting that inflation may soon be moving toward a period of relative stability. But what does this mean for borrowers, people in the process of renewing their mortgage, and homeowners more broadly? Here are some points to consider.

1.Toward a plateau in interest rates

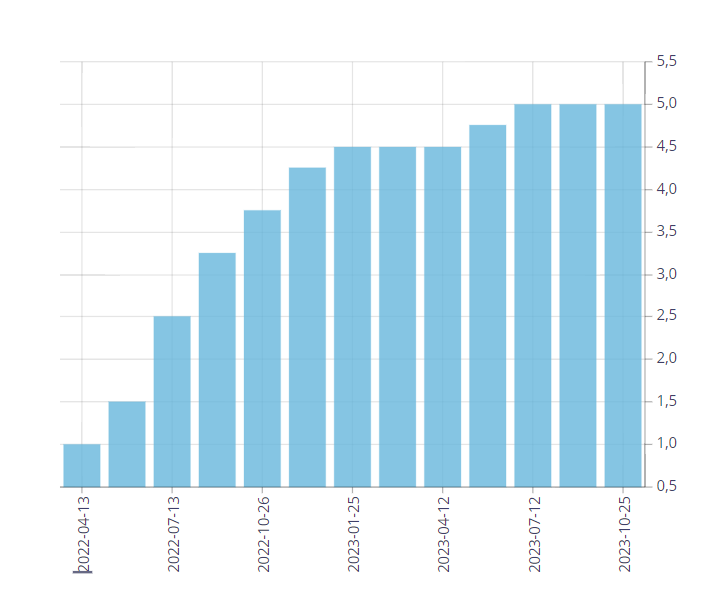

On one hand, we have experienced a significant number of rate hikes over the past year—the most substantial in decades. Since the Bank of Canada targets an overnight rate within a range of 1% to 3%, inflation could be considered under control, especially as economic growth indicators used to assess overheating inflation are showing signs of moderation. Overall, the trend appears to be moving toward stabilization. The Governor of the Bank of Canada is increasingly suggesting that we may be at the end of the interest rate hiking cycle.

The policy rate has remained stable for the past three announcements.

2.Less volatility, more competition.

When interest rates stabilize, financial institutions—whether traditional brick-and-mortar banks or virtual lenders—can afford to become more aggressive. All major financial institutions base their decisions on managing the financial risks they are exposed to. Just as you reassess your situation during rate hikes, your lender must also recalculate in order to balance its risk with its ability to lend to you. These are communicating vessels, and the entire banking ecosystem operates in this way. Much like Lavoisier’s principle: nothing is lost, nothing is created, everything is transformed.

3.The return of variable-rate products?

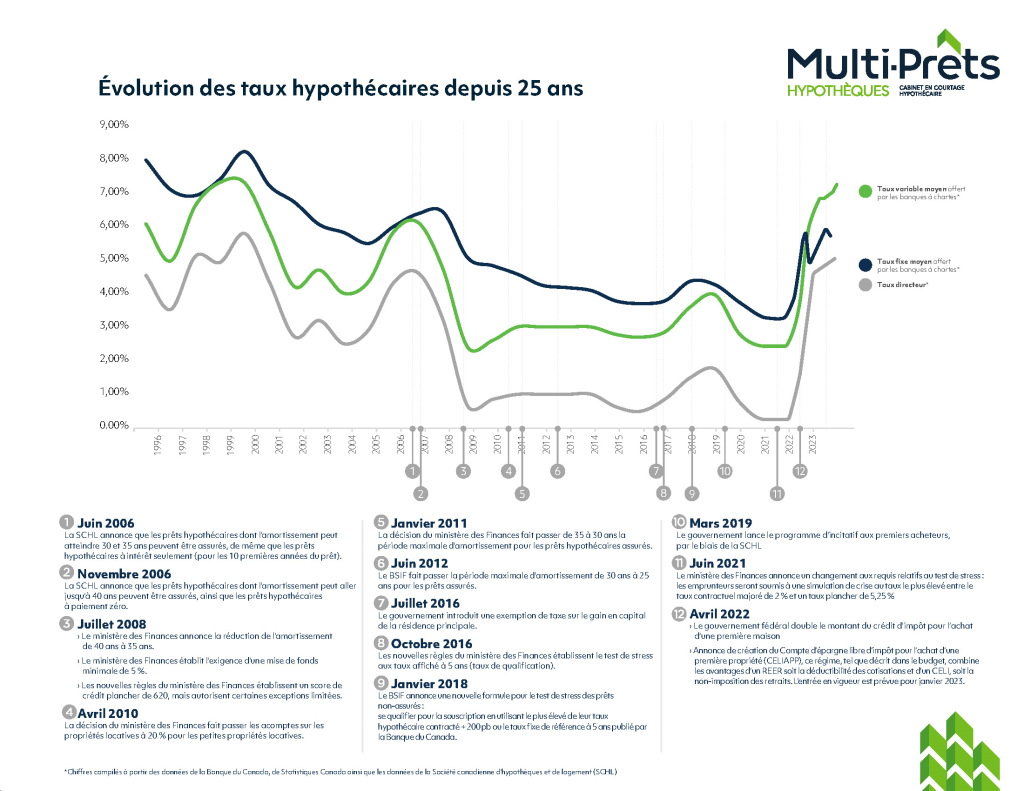

For the first time in many years, products were in an inverted yield curve situation, where fixed rates suddenly became more advantageous than variable rates. Such an occurrence is exceptional, and some even consider it an anomaly, since historically, variable rates (shown in green on the chart below) have consistently been more advantageous in the long term than fixed rates (shown in dark blue).

At the time of writing, the most competitive variable rate has dropped from 7.49% to 6.25% in just one month. Without claiming that this is a lasting downward trend, we can certainly observe a clear and realistic development.

4.An important time to compare different products.

Fixed or variable? What fits your budget? Multi-Prêts brokers compare more than 200 mortgage products from 25 different lenders.

Selecting a mortgage product is a demanding process. And contrary to popular belief, it’s not only the interest rate that matters. There are also many conditions to evaluate in order to determine whether you are truly making the best choice. It may seem obvious that comparing different mortgage products on the market is essential.

You are not required to handle lender comparisons on your own when completing your mortgage process. You can mandate a mortgage broker to carry out the comparisons and negotiate on your behalf, free of charge. With the support of an experienced professional, continuously trained and regulated by the AMF, you can rest assured.

5.You have every incentive to pay less interest.

Inflation in 2023 had a significant impact on the savings of Quebec households. Every dollar counts, especially when buying a property represents the largest share of your household budget. You need to negotiate, evaluate, and compare.

It is worth noting that nearly 70% of borrowers sign their mortgage without comparing the different products available on the market, potentially leaving thousands of dollars on the table. Our brokers compare over 200 different mortgage products for you.